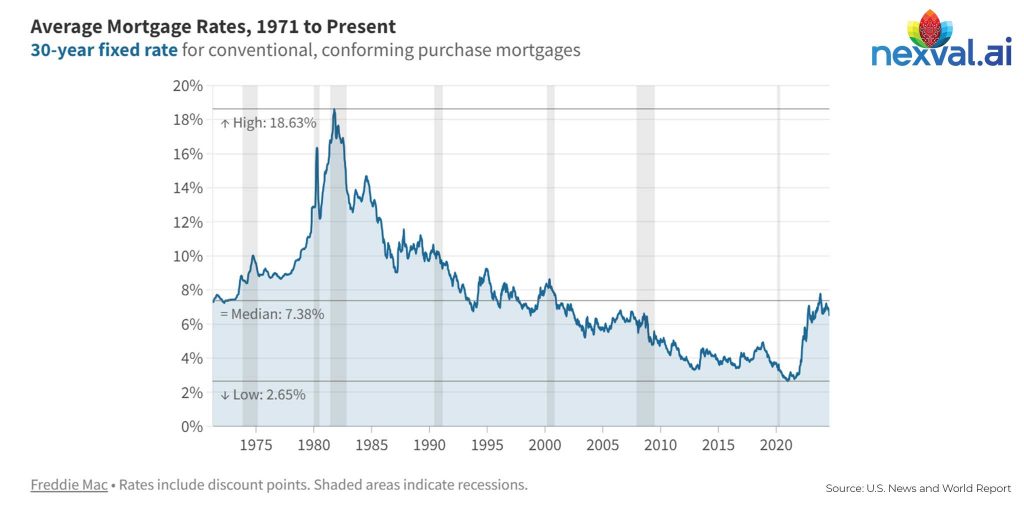

Ever since the 2008 financial crisis, we have seen the tightening of regulatory compliance rules in mortgages. COVID-19 introduced further complexities with timebound relief measures and stringent consumer protection laws. In 2024, regulatory bodies are mulling further plans to overhaul capital rules, necessitating changes in their compliance processes. How can mortgage companies keep up? Data analytics could provide an answer.

Read more: Fintech and Compliance…..a Match Made in Heaven?

The Importance of Data Analytics in Your Compliance Function

There are six reasons why data analytics could prove instrumental to the present and future of mortgage regulatory compliance:

1. Automatically ingest and process compliance guardrails as defined by regulatory bodies

Imagine the time and effort saved when you can automatically ingest and process the intricate guardrails set by regulatory bodies.

Data analytics streamlines this process by integrating sophisticated algorithms that swiftly interpret and implement regulatory guidelines into your systems. This automation ensures that your operations are aligned with the latest compliance standards, reducing the risk of oversight or error.

2. Continuously monitor your mortgage process metrics for compliance

With data analytics, you can establish a continuous monitoring system that scrutinizes every aspect of your mortgage processes in real-time.

By tracking key metrics such as loan origination timelines, approval rates, and documentation accuracy, you gain immediate insights into compliance status. This proactive approach allows you to detect deviations from regulatory requirements promptly, enabling timely interventions to mitigate regulatory compliance risks.

3. Automatically generate data reports on compliance adherence and/or deviation

Gone are the days of manual report generation and tedious data compilation. Data analytics empowers you to automate the creation of comprehensive reports that detail your compliance adherence or deviations.

These reports provide in-depth insights into your compliance posture, highlighting areas of strength and areas needing improvement. Armed with this data-driven intelligence, you can make informed decisions to enhance your compliance processes.

4. Demonstrate compliance with changing mortgage laws with concrete data-backed evidence

As mortgage laws evolve, substantiating compliance becomes increasingly challenging. However, with data analytics, you possess a powerful tool to demonstrate adherence to regulatory changes.

By leveraging historical and real-time data, you can track and analyze your compliance efforts over time. This data-backed evidence not only validates your compliance but also enables you to proactively adjust your processes to align with shifting regulatory landscapes.

5. Connect multiple data sources and data workflows to enable integrated compliance

Your regulatory compliance efforts are often hindered by fragmented data sources and disjointed workflows. Data analytics addresses this challenge by seamlessly connecting disparate data sources and workflows into a cohesive ecosystem.

Through advanced integration techniques, you can centralize data from various sources, including customer information, financial records, and regulatory updates. This integration fosters collaboration across departments and ensures consistency in compliance practices throughout your organization.

6. Detect and quantify your most persistent compliance bottlenecks using data

Identifying and addressing compliance bottlenecks is essential for optimizing your processes and minimizing risks. Data analytics equips you with the ability to detect and quantify these bottlenecks with precision.

By analyzing large datasets and identifying patterns, you can pinpoint recurring compliance issues and their underlying causes. Armed with this actionable intelligence, you can implement targeted interventions to enhance efficiency and mitigate compliance risks effectively.

Read more: How AI-Driven Analytics Can Transform Your Mortgage Processes

How to Bolster Your Data Analytics Capabilities for Regulatory Compliance

The importance of data analytics in today’s mortgage landscape simply cannot be overstated. Mortgage businesses can start preparing by implementing the following measures:

1. Conduct a data audit on your mortgage function

Begin by conducting a comprehensive data audit on your mortgage function. Evaluate the quality, accuracy, and completeness of your data across all stages of the mortgage lifecycle. Identify any gaps or inconsistencies in your data collection and storage processes.

This audit will provide you with valuable insights into the current state of your data infrastructure and help you identify areas for improvement to ensure regulatory compliance.

2. Analyze regulatory requirements across jurisdictions and identify data correlations

Regulatory requirements vary across different jurisdictions, making it essential to analyze and understand these requirements thoroughly. Utilize analytics to identify correlations between regulatory mandates and specific data points within your mortgage operations. By mapping out these correlations, you can tailor your data analytics strategies to ensure compliance with relevant regulations in each jurisdiction you operate in.

3. Invest in a compliance team or outsourcing firm with data competencies

To bolster your data analytics capabilities for regulatory compliance, consider investing in a dedicated compliance team or outsourcing firm with expertise in data analytics. These professionals can assist you in developing and implementing data-driven compliance strategies, leveraging advanced techniques that may be outside your existing skills portfolio.

Collaborating with experts in data analytics will enable you to stay ahead of evolving compliance challenges and maintain regulatory compliance effectively.

4. Instill the importance of data analytics in your operational culture

Foster a culture within your organization that prioritizes the importance of data analytics for regulatory compliance. Educate your employees – i.e., provide training on data analytics tools and techniques. By embedding data analytics into your operational culture, you can cultivate a proactive approach to compliance management and empower your team to leverage data effectively in their day-to-day activities.

5. Strengthen cloud-based infrastructure for more agile data operations

Cloud computing offers numerous benefits for data analytics, including flexibility, scalability, and accessibility. By migrating your processes to the cloud, you can streamline data storage, processing, and analysis, enabling faster decision-making and more efficient compliance management.

Additionally, cloud-based solutions often come with built-in security features and compliance certifications, helping you ensure data privacy and regulatory compliance.

Read more: Navigating Compliance Challenges: How a Mortgage Quality Control Partner Can Help

Research shows that 85% of mortgage businesses are concerned about being in compliance; just 15% are confident about regulatory compliance in 2023-24. By harnessing the power of data and recognizing the importance of data analytics, you can stay ahead of the curve and update your tools and processes to address ever-changing regulatory concerns.

Speak to Nexval’s experts to learn how.